In this months’ Singal issue we dive into the latest insights from our Global Project Tracker in the new report ‘Clean industry: transformational trends’.

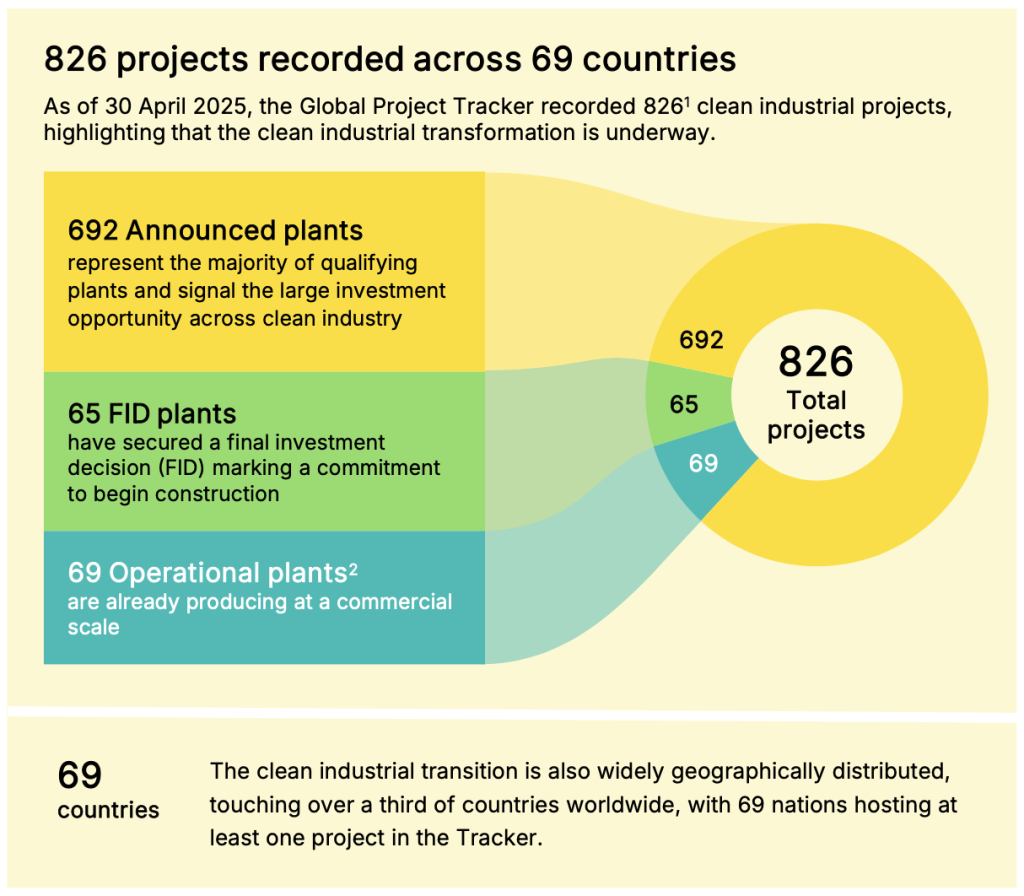

As we reach the half-way point of the year, we’re seeing more opportunities for clean industry. Despite geopolitical headwinds and macro-economic uncertainty, our Global Project Tracker now counts a record 826 commercial-scale clean industrial projects across 69 countries.

This encouraging news is just one of the many datapoints fresh from the third edition of the Global Project Tracker and informs the insights in our Clean industry: transformational trends report.

We’re covering some of the key findings in this special edition of Signal:

Faustine Delasalle discussing the Global Project Tracker insights during LCAW

Since the beginning of the year, we have been living through a whirlwind of global geopolitical and economic changes. The last few weeks were no exception, with military conflicts, tariffs, and heatwaves making headlines. It takes a good dose of stubborn optimism to keep seeing and seizing opportunities in that storm. But I reach the mid-year point confident that these opportunities exist, including in clean industry.

It’s one year on from the publication of our first Global Project Tracker and with the latest update we can see that clean industry transformation is on the way – the ‘new industrial sunbelt’ (more on this below) is driving a diversification of industrial centres across the globe and the pipeline of commercial-scale, clean industrial projects is rapidly expanding. If every project in it were to go into operation that would mean a reduction of around 1 Gt of CO2 emissions per year. It would also unlock $1.6 tn of investment, with more than half flowing in emerging markets and developing economies, open-up new win-win trade relationships between regions with different competitive strengths, and in turn would bring huge socio-economic benefits.

Hot on the heels of our report, London Climate Action Week kicked off, more packed than usual. Three things stood out for me throughout the week:

Faustine Delasalle

CEO Mission Possible Partnership I Executive Director Industrial Transition Accelerator

As we revealed in June, a total of 826 clean industrial plants around the world have now been announced, reached final investment decisions (FID) or gone into operation.

These projects span nearly 70 countries and appear on every continent of the world. Eight plants have reached FID in the past six-month period bringing the total number of commercial-scale FID or operational plants globally to 134. A milestone 692 are announced and keen to move towards construction but must first secure investment.

Across sectors some are moving faster than others, with rapid progress in chemicals coming from clean ammonia and methanol – used in established industrial processes and emerging as clean fuel contenders in the shipping sector. Together, they make up 70% of all announced projects and 35% of all projects past FID.

Ammonia, used for fertiliser production and vital for food security, stands out in particular as the most advanced sector in terms of ambition, with an announced pipeline over twice the size of the next most promising sector (aviation) and with 28 FIDs – the most of any sector.

Source: Mission Possible Partnership June 2025, Clean industry: transformational trends

Also in fuels, the aviation industry is progressing steadily, with 22 sustainable aviation fuel (SAF) plants in operation and an encouraging array of proposed projects that make up 20% of the total clean industry pipeline. OMV Petrom’s SAF Refinery in Petrobrazi, Romania is one of the latest plants to reach FID in this period and will become one of the first commercial-scale producers of this clean fuel in Southeastern Europe. The EU makes up 24% of aviation capacity past FID and 15% of announced capacity.

And as our new report Clean Industry: Transformational Trends shows, clean industry has reached a significant milestone with close to 700 projects announced representing a $1.6 trillion investment opportunity and a chance for new industrial regions to emerge.

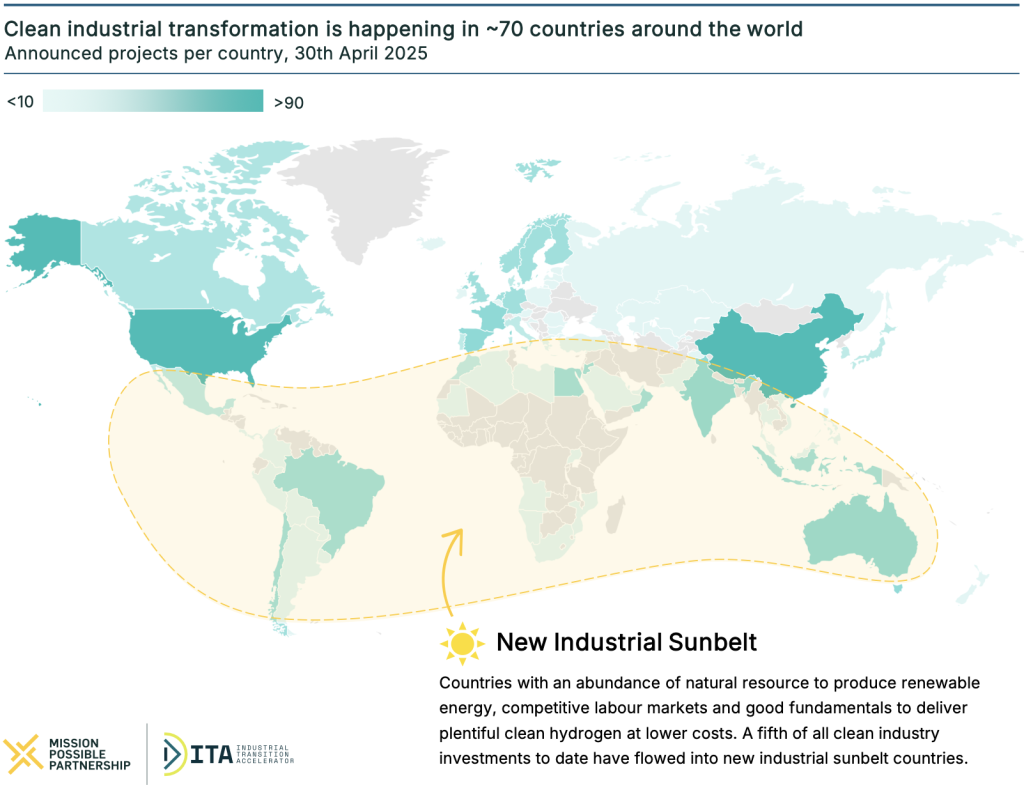

China is still the frontrunner in clean industry development, with a quarter of the $250 bn of ring-fenced investment in clean plants to date, closely followed by the US at 22% and the EU at 14%. But the latest data shows that a diversification of industrial centres is happening and a ‘new industrial sunbelt’ is catching up.

This bloc of emerging markets, which includes India, Egypt, Brazil, Chile and Oman, is set to seize the clean industry opportunity and expand the world’s industrial bases: it already holds a fifth of current financing and over half of the entire investment pipeline.

Why the ‘new industrial sunbelt’?

These are countries with an abundance of natural resources to produce renewable energy, competitive labour markets and good fundamentals to deliver plentiful clean power at lower costs. It comprises countries in the Middle East, Africa, Latin America, Asia and Australia.

Source: Mission Possible Partnership June 2025, Clean industry: transformational trends

Of the massive $1.6 tn investment opportunity inherent in the 700 clean projects announced globally, $950 bn (59%) of this falls in sunbelt countries with a $775 bn opportunity sitting with emerging markets and developing economies.

Investment here can boost domestic and foreign direct investment, open new industrialisation opportunities, aid the modernisation of local infrastructure, upskill the local workforce and transition economies from carbon-intensive to sustainable growth models.

Critically, clean ammonia production is increasingly shifting to sunbelt emerging markets and developing economies (EMDEs) – home to half of the total clean ammonia pipeline capacity.

And production costs for clean ammonia are expected to fall further and faster in sunbelt countries than others, opening opportunities for countries with historical industrial bases – but higher production costs – to join forces. Falling green ammonia costs here could lead to the emergence of new trade corridors as existing industrial nations seek to spread and secure a reliable supply.

Drawing on analysis of clean industry projects that have successfully reached FIDs, the Global Project Tracker insights also delve into the common success factors that can help projects reach bankability and attract financing, all of which can strengthen the prospect of operationalising the pipeline.

Energy and capex cost reductions

Cheap and abundant renewable power is the success story of the past decade and the maturing of this market is creating a positive knock-on effect for industry transformation. Continuing declines in the cost of solar panels, battery energy storage systems and other clean energy technology are a tailwind supporting electrification and green hydrogen-related projects.

Beyond the sinking capital expenditure (capex) costs due to technology maturity, most sunbelt EMDEs benefit from lower capex costs, which will boost bankability for much of the pipeline.

Demand measures create market certainty

Securing reliable demand through off-take agreements for low-carbon commodities is also critical for project bankability as these provide revenue certainty, reduce market risk and help build a strong business case.

While early agreements were driven by voluntary corporate commitments, market scale-up now increasingly relies on regulatory tools. For example, the EU’s aviation fuel mandate requires 2% sustainable aviation fuel by 2025 and 6% by 2030. New shipping emissions reduction guidelines from the International Maritime Organisation and embodied carbon limits in construction are also starting to create some levels of demand certainty.

However, demand measures remain geographically concentrated, creating risks for projects worldwide.

Policy support crucial for enabling projects

Stable and supportive government policy plays a crucial role in enabling clean industry. Support on capex – including government subsidies, tax credits and financial guarantees – is essential for enabling capital-intensive projects, while support on operational expenditure -mechanisms like Contracts for Difference – can provide price certainty for outputs and help Carbon pricing also enhances economic viability, for example with the EU’s €80 per tonne CO2 price creating favourable conditions for steel and cement projects.

The Clean Industry: Transformational Trends report demonstrates that success occurs where all three drivers of, capital costs, boosting demand and policy support combine effectively.

Download your copy now for a deep dive into these and further insights, as well as a sector snapshot overview of all clean industry sectors in the pipeline. Explore the Global Project Tracker.

Over 800 clean industrial plants are being planned, built or are operating globally, with chemicals and fuels leading. Bringing the entire pipeline online will require five times more investment than has been secured to date. To explore the data in more detail and find out what progress your sector or region is making please visit – Global Project Tracker.

Hear more from MPP at events and access tickets on related conferences from our partners.

Thank you for reading, if you enjoyed this newsletter, please share it with your network.

If this edition of Signal was shared with you, you can sign up for our monthly mailings here.

The Mission Possible Partnership Team