In this month’s issue of Signal we took a tour of Heidelberg Materisl’s Brevik retrofitted cement plant, analysed the investment opportunities in Asia and Oceania, and looked at Brazil’s sustainable aviation prospects.

Around the world, Europe leads the way on first-of-a-kind projects but emerging markets and developing economies are gaining pace with developed countries on the proportion of industrial decarbonisation projects in development. This month’s Signal reflects this with reports on historic developments in all corners of the globe, including:

Faustine Delasalle at the Heidelberg Materials’ Brevik plant

This April I was in Norway where I attended a conference bringing together philanthropic funders, NGOs, and industry groups working on cement and concrete decarbonisation. By far the highlight of the trip was our visit to Heidelberg Materials’ Brevik plant, the first cement plant ever worldwide to be retrofitted with CCS. It will start operating in June this year.

Some interesting data: the plant will produce 1.2Mt of cement per annum (enough to build several bridges or dams) and will capture 50% of its CO2 emissions (400kt pa), leveraging waste heat from the kiln for the capture process. This is equivalent to roughly 35% of total emissions from the cement industry in Norway. The carbon captured will be liquified at -26C, shipped and then pumped 2,600 metres, or just over two and a half kilometres, below the seabed, in a carbon store that is currently designed to absorb 1.5Mt per annum. Eventually this storage will be expanded to a capacity of 5Mt per annum, one tenth of the EU’s target for carbon stored annually by 2030.

First-of-a-kind plants take a loooong time to come to fruition. In Brevik, the first pre-feasibility studies started in 2005, the full feasibility study was done in 2016, the FEED (front end engineering design) in 2018, construction started in 2021 and the plant will finally be operational later this year – so a 20-year journey. The good news is the timeline for the next-of-a-kind plants can be sped up and Heidelberg estimates it will be a mere four to five years for their next projects… if not delayed by planning and permitting intricacies.

I’ve always been impressed by the leadership of Heidelberg Materials’ Chairman, Dominik von Achten, who we have the great privilege of having on Mission Possible Partnership’s board. He is personally committed to making environmental sustainability a driver of business success with the proof being that already 40% of the company’s revenues come from sustainable products – lower-carbon products, recycled products and services to improve materials efficiency, while the company keeps delivering strong financial results every quarter.

Across the sea in London, another significant milestone took place in April: After many months and many discussions an initial agreement was made on shipping’s energy transition at the International Maritime Organization’s 3rd Marine Environment Protection Committee meeting with the majority of countries voting in favour of the new measures. Although slightly convoluted and still imperfect, the carbon pricing mechanism that the IMO envisions should provide first incentives for shippers to reconsider their fuel mix and is a signal of hope for multilateral climate action, at a time when multilateralism is under pressure.

This milestone also matters for the transformation of the whole global industry and transport system – far beyond shipping. Why? Driving uptake of clean shipping fuels, in particular clean ammonia, can️ bring down carbon emissions from shipping, but also importantly trigger a scale-up of the production of clean hydrogen, which can help push the cost of clean hydrogen down, which will then benefit many other industry and transport sectors, including fertilisers, chemicals, steel and aviation.

Faustine Delasalle

CEO Mission Possible Partnership I Executive Director Industrial Transition Accelerator

Pertamina’s Cilacap Green Refinery, Indonesia. Image @ Pertamina

Across Asia and Oceania, a whopping 109 clean industrial plants are seeking investors while a raft of new government initiatives are starting to provide incentives for sustainable commodity production: the last 12 months have seen an uptick in sustainable aviation fuel (SAF) projects across Southeast Asia and notable government support for clean iron ore projects.

Southeast Asia’s most attractive subsector?

The SAF pipeline is advancing at pace in Southeast Asia, to meet both a rising consumer demand for travel and recent mandates. Four new projects were announced in the second half of 2024, spurred by a mix of state mandates and corporate ambition. From 2026, Singapore will introduce a fixed SAF levy on all aviation ticket prices, with the money going to central procurement of SAF by Singapore’s aviation authority.

Meanwhile, Indonesia’s Pertamina Cilacap plant is due to finish construction in 2026 and seeks investment for a second phase to boost domestic SAF supplies to meet a 5% SAF mandate in 2025. Japan’s upcoming 10% SAF blending mandate has also prompted two major collaborations to supply SAF from Malaysia.

Government support boosts clean metals across the region

2025 has also brought a raft of support for clean production of metals, including Japan’s rebate for EV manufacturers using green steel and Australia’s $1bn Green Iron Investment Fund for new facilities and supply chains, along with a $2bn Aluminium production tax incentive.

Across sectors, outside of China, India is leading with the highest proportion of projects seeking investors. It’s notable due to federal and state initiatives including a steel sector roadmap, plans for a carbon market by mid-2026, the National Green Hydrogen Mission, which promotes clean industrial hubs, production incentives for electrolysers and green ammonia procurement mechanisms and Infrastructure Investment Trusts.

In contrast Japan, which despite its high ambitions and considerable state support, also has many plants seeking investment but no commercial scale facilities under construction yet due to insufficient low-cost clean power. South Korea shows strong progress with plans for eight additional commercial-scale plants and its Green New Deal, which aims to transition the country towards a low-carbon economy and focuses on green hydrogen, storage and grid infrastructure.

Further steps for governments

Governments can boost investment by stimulating demand for green commodities through quotas, mandates and public procurement prioritising low-carbon commodities. Building regulations with embodied carbon limits can also trigger demand from end users, while tax credits and loan guarantees have also proved effective in other markets.

Green Market Makers (GMMs) also offer significant potential as public-backed intermediaries for low-carbon commodity trading – bridging cost differences and absorbing offtake risks. The first Asia Pacific GMM could emerge from Japan and South Korea collaborating on green steel tenders, potentially partnering with Australia to leverage its huge renewable energy potential.

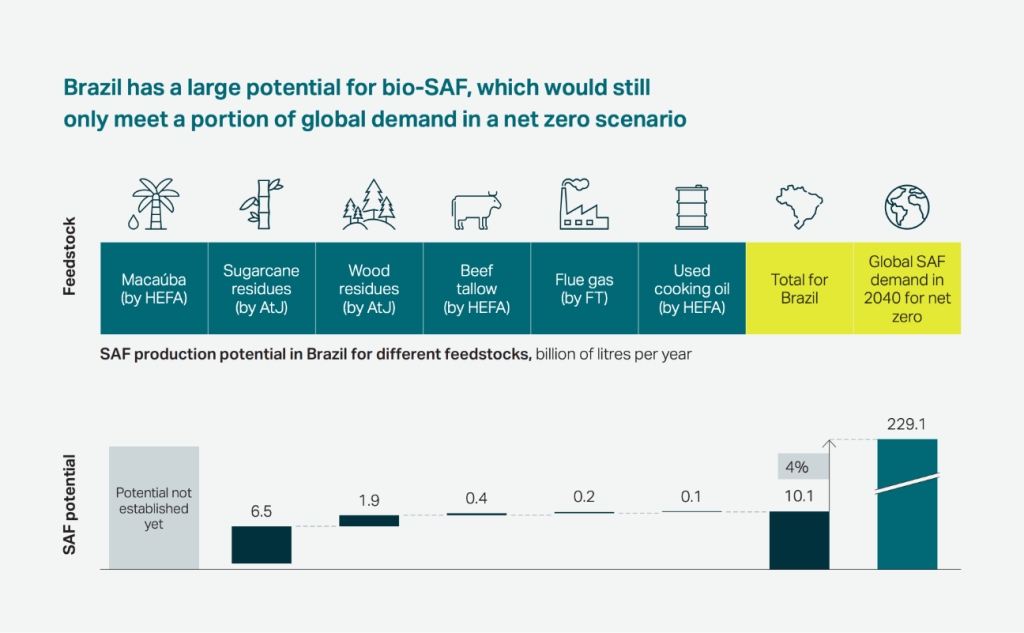

After delving into low-emissions steel and chemicals in Brazil with the country’s Industrial Transition Accelerator (ITA) Project Support Programme, the final part of this mini-series takes a snapshot of Sustainable Aviation Fuel (SAF) in the country.

The aviation sector contributes over 2% of global CO2 emissions, with decarbonisation efforts increasingly focusing on SAF as the most promising near-term solution: Unlike electrification or green hydrogen, SAF provides a drop-in fuel solution with the necessary energy density for long-distance flights – making it crucial for the industry’s emissions reduction strategy.

Brazil is very well-positioned to become a leading SAF producer, leveraging its abundant renewable energy resources and status as the world’s top bioenergy producer. This comes as regulations like the EU’s ReFuelEU Aviation rules and Brazil’s Fuel of the Future law create market potential for SAF producers, with EU targets rising from 2% in 2025 to 70% by 2050.

The first SAF production route, Hydro Processed Esters and Fatty Acids (HEFA), converts bio-oils into aviation fuel using mature biodiesel production technologies. Brazil is exploring innovative feedstocks like macaúba, a palm tree species that can be grown on degraded land – addressing sustainable feedstock challenges through integrated crop-forestry systems.

The second is Alcohol-to-Jet (AtJ), which converts ethanol into SAF, with second-generation ethanol from the residues of sugarcane production being the primary feedstock.

The third route, Power-to-Liquid (PtL or e-SAF), involves converting renewable electricity into green hydrogen and then combining it with captured carbon to produce SAF, a process for which Brazil’s extensive wind and solar resources make it ideally suited.

Brazil’s bio-SAF potential. ITA Brazil Insights Briefing

HEFA SAF on the rise, challenges to overcome

The ITA has identified three major SAF projects in Brazil: Acelen Renewables’ project with 0.93 mega tonnes per annum (Mt pa), Petrobras’ Polo Gaslub with 0.88 Mt pa and Petrobras’ RPBC project with 0.70 Mt pa. All employ HEFA technology and plan to use feedstocks including macaúba oil and various vegetable and animal-based inputs.

However, Brazil’s pipeline of announced SAF projects lags that of other regions around the world, indicating there remain challenges to capitalising on this potential.

Demand creation and establishing support for long-term offtake agreements are both needed, the first to overcome SAF’s significant green premium and stimulate market adoption, and the second to create investor confidence as well ensure long-term viability of SAF projects.

Sustainability certification for export is also crucial, to show clear traceability of organic feedstocks for international standards like those of the International Civil Aviation Organization (ICAO) – and prevent potential biodiversity loss or increased carbon emissions.

Securing sufficient supply volumes of feedstock is also a substantial logistical challenge and technology maturity remains a critical hurdle – both within Brazil’s early-stage SAF production environment and with AtJ and e-SAF technologies still in development stages.

By addressing these challenges systematically, Brazil can become a key player in the bio- and e-SAF market, leveraging the competitive production cost of hydrogen and abundant bioresources. And it’s exactly these kinds of systematic challenges the ITA is targeting in efforts to mobilise stakeholders and create better investment conditions for selected projects.

In addition to the chemical and steel sector focuses of the last months, you can also access deep-dives into Brazil’s cement and aluminium sectors in the full Brazil Insights Briefing from ITA. We’ll be back with more updates on the support programme in the near future.

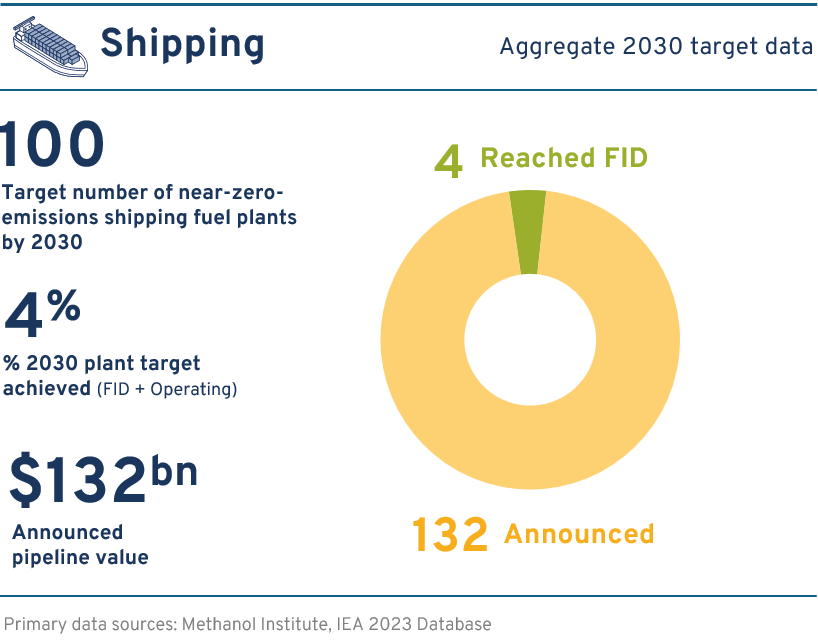

Pipeline progress for clean shipping

The volume of announcements show huge ambition for low-carbon shipping but challenges remain in changing engines and associated infrastructure. Check out our Global Project Tracker for more project information and look out for the latest Tracker updates coming very soon.

Global Project Tracker, Mission Possible Partnership

Hear more from MPP at events and access tickets on related conferences from our partners.

Thank you for reading, if you enjoyed this newsletter, please share it with your network.

If this edition of Signal was shared with you, you can sign up for our monthly mailings here.

The Mission Possible Partnership Team