In this month’s edition of Signal we explore why clean assets are becoming strategically critical – and we shine a light on some of MPP’s work around the world to accelerate that change.

Recent geopolitical shocks are making the case for accelerating clean industry development increasingly clear. As we prepare to publish the next Global Project Tracker in early June, there are signs that governments, businesses and investors are recognising the value that clean industrial assets can bring to long-term stability.

Contents

Beyond the devastating human tragedy, the rapid escalation of conflict in the Middle East is a reminder of how exposed many economies still are to fossil fuel shocks and fragile supply chains.

We are seeing the consequences of this exposure play out quickly. Energy price spikes feed through into transport and industry, fertiliser supply chains and then food production, fuelling inflation. If they last, oil and gas supply disruptions could lead to shortages in vulnerable countries, disrupting daily lives, economic activities, and importantly food supply chains.

75% of the world’s population lives in countries that are net importers of fossil fuels. For these countries, this is not just a brief disruption they can shrug off. It is a structural vulnerability that has significant costs, both human and economic.

Energy and food security are now at the centre of conversations across the world. And increasingly, those conversations are turning towards the role of the clean industry transition in national resilience strategies.

The logic is straightforward. Countries that can produce essential fuels, chemicals, and materials using domestic clean energy – sometimes combined with diversified clean energy imports – reduce their exposure to concentrated and volatile fossil fuel imports. They are better placed to absorb external shocks. We observe these opportunities across our global portfolio.

This is particularly visible in fertilisers. Rising energy costs intensify nitrogen fertiliser shortages, which in turn threaten crop yield and food security. We can already see these risks affecting India and Brazil – two of the world’s largest agricultural producers – who depend heavily on imports from the Middle East. However, our work on the ground in both countries indicates that they can mitigate similar risks in future by using their growing renewables capacity to produce green fertilisers domestically, both reducing exposure to global shocks and building new engines of industrial development with spillover effects in other industrial sectors.

Meanwhile, transport fuel security is uppermost in the minds of many policymakers. Australia, for example, imports around 90% of its refined fuels, leaving it exposed to supply disruption. But it has the resources to change that equation. We are supporting a growing pipeline of biofuel and e-fuel projects, which could strengthen domestic supply and improve resilience, all while developing a new industrial sector that could eventually serve the emerging sustainable aviation and maritime fuels market across Asia-Pacific.

In Europe, successive energy crises have exposed the vulnerability of industry – particularly energy-intensive sectors reliant on imported gas or electricity markets where prices are set by gas. The clean transformation of the chemicals and metals industry, underpinned by a mix of clean energy sources – local production, production in European countries with ample renewable potential (e.g. Scandinavia and Iberia), and diversified imports from trusted trade partners – is a clear route to greater energy security and more resilient industrial supply chains.

What is striking is both how consistent the case for future-proofing economies through a shift to clean industry has become, and how difficult it remains for companies to pursue this necessary transformation in the midst of crises that disrupt their business.

The opportunity for countries to navigate a more uncertain and volatile global economy is clear. Turning it into reality requires billions in investment into clean industrial assets – investments which will not happen without decisive government intervention to de-risk them, in particular by creating greater market certainty through regulation. Decisions taken today will shape how countries cope when the next crisis comes.

Faustine Delasalle

CEO Mission Possible Partnership I Executive Director Industrial Transition Accelerator

With a clean industry project pipeline similar in size to India’s and behind only China and the US, Australia is perfectly positioned to capitalise on its considerable natural resources. Our newly published briefing highlights the enormous economic opportunity on offer, if the right policies are put in place.

This is the first clean industry spotlight of Build Clean Now, our global campaign that showcases the countries and companies already seizing opportunities, shows where near-term potential is strongest, and builds momentum around the solutions that can unlock major projects.

Published at Climate Action Week Sydney in March, the briefing emerged from a workshop in October 2025 of senior clean industry leaders in Australia, including project developers, federal and state government representatives and investors.

It assesses Australia’s clean industry pipeline, what’s preventing projects from reaching final investment decision (FID), and how to accelerate production of new products such as clean iron, green ammonia, high value chemicals and sustainable fuels. This shift will unlock a substantial economic opportunity and create jobs in legacy industrial regions like Gladstone in Queensland.

Workshop participants agreed that common barriers include buyers unwilling to pay a premium for green products, policy uncertainty, fragmented demand and high upfront capital costs. These make it difficult to generate long-term offtake agreements and financing.

To unlock billions in private investment and accelerate progress, the government should consider:

MPP and partner Cyan Ventures hosted a discussion on investing in clean industry at Climate Action Week Sydney last month.

“Australia is home to one of the largest clean industrial pipelines in the world,” said Rachel Howard, MPP’s Director of Asia-Pacific. “This can translate into huge economic and social benefits across the country, while supporting the path to net zero. To achieve that, we need true collaboration between government, industry and finance to create a blueprint that can be replicated around the world.”

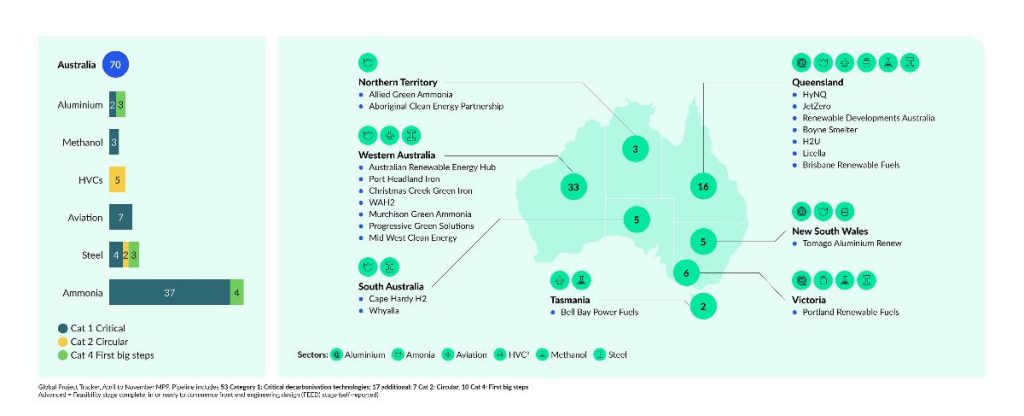

Australia has 70 projects in development – including 15-20 at an advanced stage – behind only China and the US. These projects could bring in more than AUD290 billion in investment if the government uses measures such as mandates, public procurement and revenue certainty mechanisms to stimulate demand.

The first steps are already being taken. The government’s Future Made in Australia agenda will invest AUD22.7 billion over the next decade in strengthening competitiveness via clean industries. In the private sector, Qantas’ Climate Fund – the world’s largest aviation fund for climate change – is investing over AUD290 million in sustainable aviation fuel (SAF), and Fortescue, Progressive Green Solutions and Green Steel WA are pushing forward with iron projects.

Pete Hemingway, Senior Associate, Low Emissions Standards for the Industrial Transition Accelerator (ITA)

MPP’s Pete Hemingway has joined the ISO–GHG Protocol Joint Working Group, which is developing a new international standard for carbon footprint of products.

The group comprises nominated experts from the standards community and is tasked with replacing ISO 14067 and the GHG Protocol Product Standard with a single, co-branded standard, consolidating two widely used tools in product-level GHG accounting.

Harmonised standards give manufacturers, investors, policymakers and consumers a credible basis to differentiate lower- and higher-emission products, reduce trade friction, and accelerate clean market growth.

Building on our new partnership in India, the ITA and GH2 India brought together policymakers, developers and certification bodies in New Delhi last week to tackle a critical issue for India’s clean hydrogen pipeline: how projects can meet EU requirements on Renewable Fuels of Non-Biological Origin (RFNBOs), a category that includes green hydrogen and its derivatives such as ammonia and synthetic fuels.

While technical, the implications are immediate. Clarity on these rules will determine whether Indian projects can access European markets – and whether they can secure the long-term offtake and financing needed to move to investment.

Discussions focused on practical pathways to address geographic correlation requirements, with growing alignment around solutions that reflect how India’s power system actually operates, including recognition of a single integrated national electricity market and the role of long-term power purchase agreements.

Across the conversation, one message was clear: progress now depends on regulatory clarity and pragmatic interpretation. Without it, projects face uncertainty. With it, India has a clear opportunity to position itself as a competitive supplier of clean hydrogen and derivatives to global markets.

The ITA will continue working with partners to translate these insights into actionable guidance, including further engagement with certification bodies and policymakers at the World Hydrogen summit in Rotterdam in May.

India has one of the world’s largest clean industrial pipelines. For more detail on what’s possible, take a look at the ITA’s publication from November 2025: Unlocking India’s Clean Industrialisation Opportunity

Australia’s opportunity: 70 clean industry projects in development across the country could unlock nearly AUD300 billion in investment.

Of the 70 projects, 53 fall into Category 1: Deep decarbonisation. Of the 17 additional projects, seven are Category 2: Circular solutions and 10 fall into Category 4: First big steps.

Explore the data and read more about the progress of these different solutions in our Global Project Tracker.

Hear more from Mission Possible Partnership at events and access tickets on related conferences from our partners.

Thank you for reading, if you enjoyed this newsletter, please share it with your network.

If this edition of Signal was shared with you, you can sign up for our monthly mailings here.

The Mission Possible Partnership Team